Innovation drives long-term economic growth

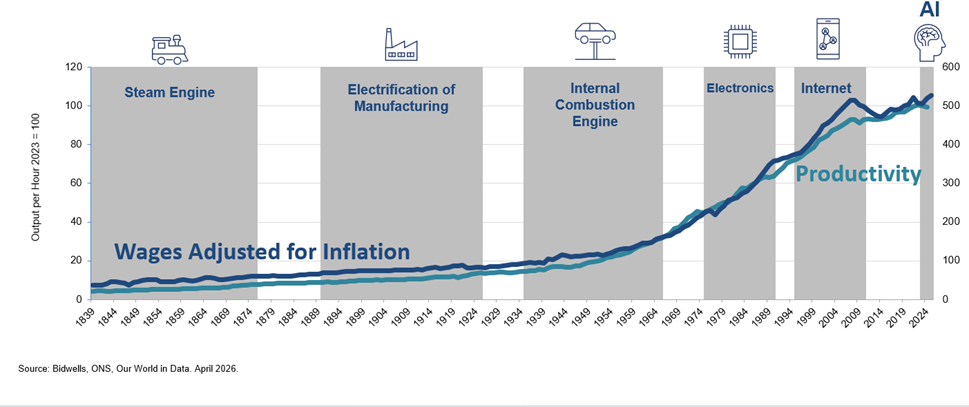

Historically the introduction of new technology has boosted productivity by enabling companies to launch new products and make existing goods and services more efficiently and cheaply. Between 1839 when Bidwells was founded and 1939, productivity in the UK grew steadily by 1.3% p.a. as new inventions such as the steam engine and later electric motors were adopted and production processes were re-organised to make best use of them.

Productivity growth then doubled to 2.9% p.a. in the second half of the 20th century, as international competition intensified and UK businesses became more willing to adopt new technology. However, productivity growth over the last 19 years since 2007 has been much slower, probably because tighter financial regulation since the GFC has inhibited investment. A similar slowdown has been seen in other developed economies. One argument is that recent digital innovations, social media, smartphones, the consumer internet, have changed our daily lives more than they have changed how businesses operate. The big question is whether AI is different.

Productivity matters because over the long-term it determines the wages employers can afford to pay and by extension, government tax revenues and perceptions of whether politicians are delivering on promises to make people better off. One of the reasons for the current disenchantment with mainstream political parties is that real wages are barely higher now than in 2007. To misquote Paul Krugman Innovation isn’t everything, but in the long run it is almost everything.

UK Productivity and Wages Adjusted for inflation

Innovation is accelerating

Another feature of technology apparent from the chart is that the pace of innovation is accelerating. It took 75 years for the telephone to reach 50 million users, but less than 2 months for ChatGPT. We often think of the launch of ChatGPT in November 2022 as the dawn of AI, but in truth the technology has been employed in several areas since 2017-18 including facial recognition, drug discovery, fraud detection and robotics.

Innovation and employment

The impact of innovation is also clear when we look at recent trends in employment, with information technology and life science seeing the fastest growth over the last decade. In reality the impact of innovation is greater than the data suggest, because spending by companies and staff in information technology and life sciences has supported employment in other sectors such as professional services, hospitality and construction.

Estimates suggest that every 10 new jobs in knowledge intensive industries generates an additional seven jobs in the rest of the economy. However, on the downside, the decline in employment in manufacturing, retail and publishing, in particular newspapers, is a reminder that new technology can destroy as well as create jobs.

One characteristic of both tech and life science sectors is that companies tend to locate close to universities and research institutes where there is a pool of skilled labour, and once a cluster is established it can become self-perpetuating, attracting companies and scientists from other cities and countries. London has accounted for 60% of the growth in tech jobs over the last decade, while a quarter of all new life science jobs were in the Ox-Cam Corridor. Unfortunately, that concentration means that many other towns and cities have largely missed out on the gains from innovation.

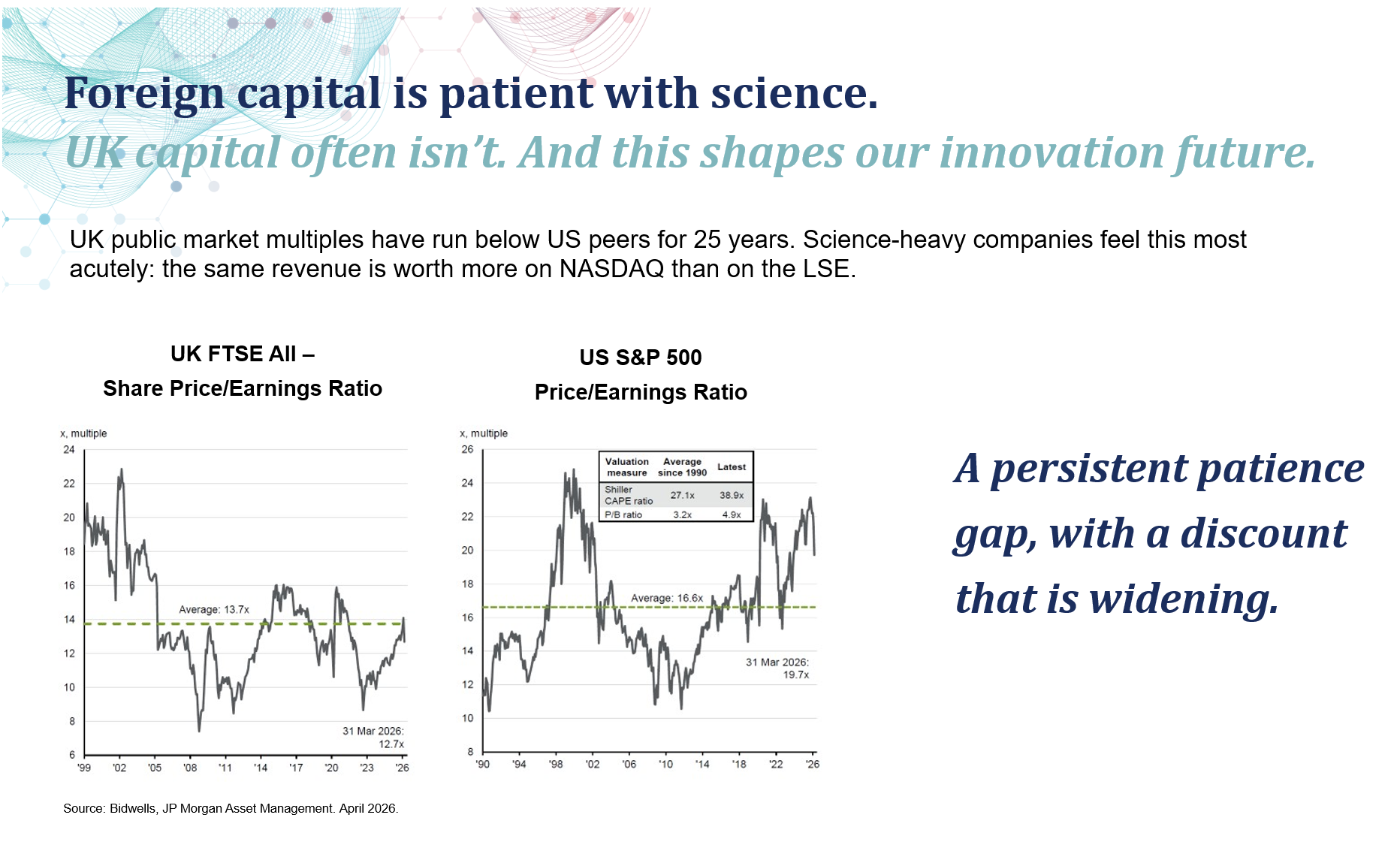

Foreign investors value our research more than we do

In general, foreign and in particular US investors, are more enthusiastic about science and tech businesses than UK investors and are prepared to pay higher prices. Although not strictly comparable, the long-term average price/earnings ratio for US equities is around 20% higher than the p/e ratio for UK equities. As a result, some UK start-ups relocate to the US where it is easier to raise capital and many others stay, but are later bought out by foreign companies and investors.

The relocation of dynamic, new businesses is clearly negative for the UK economy, but what about the sale of UK based businesses to foreign owners? On the plus side multi-nationals can provide new capital for expansion, open doors to new markets, and take on a lot of the support functions required to run a business. The original founders of the business may also use the proceeds from the sale to fund new UK start-ups, increasing the supply of local seed and venture capital.

DeepMind, which is a leader in AI, is a positive example of foreign ownership. Since its acquisition by Google, now Alphabet, in 2014, its London workforce has grown from 75 to over 1,000. Founder Demis Hassabis was awarded the Nobel Prize in Chemistry in 2024 for his work in predicting protein structures, and hundreds of former employees have founded or joined other UK start-ups. Just last week, DeepMind’s spin-out Isomorphic Labs raised $2.1 billion led by Thrive Capital, with the UK Sovereign AI Fund among the backers.

The DeepMind example is however unusual. Most acquisitions deliver less for the UK. The acquired company may lose control over its R&D, which has wider implications for research relationships across the cluster, while profits generated in the UK will be repatriated, rather recycled into new investment within the domestic ecosystem

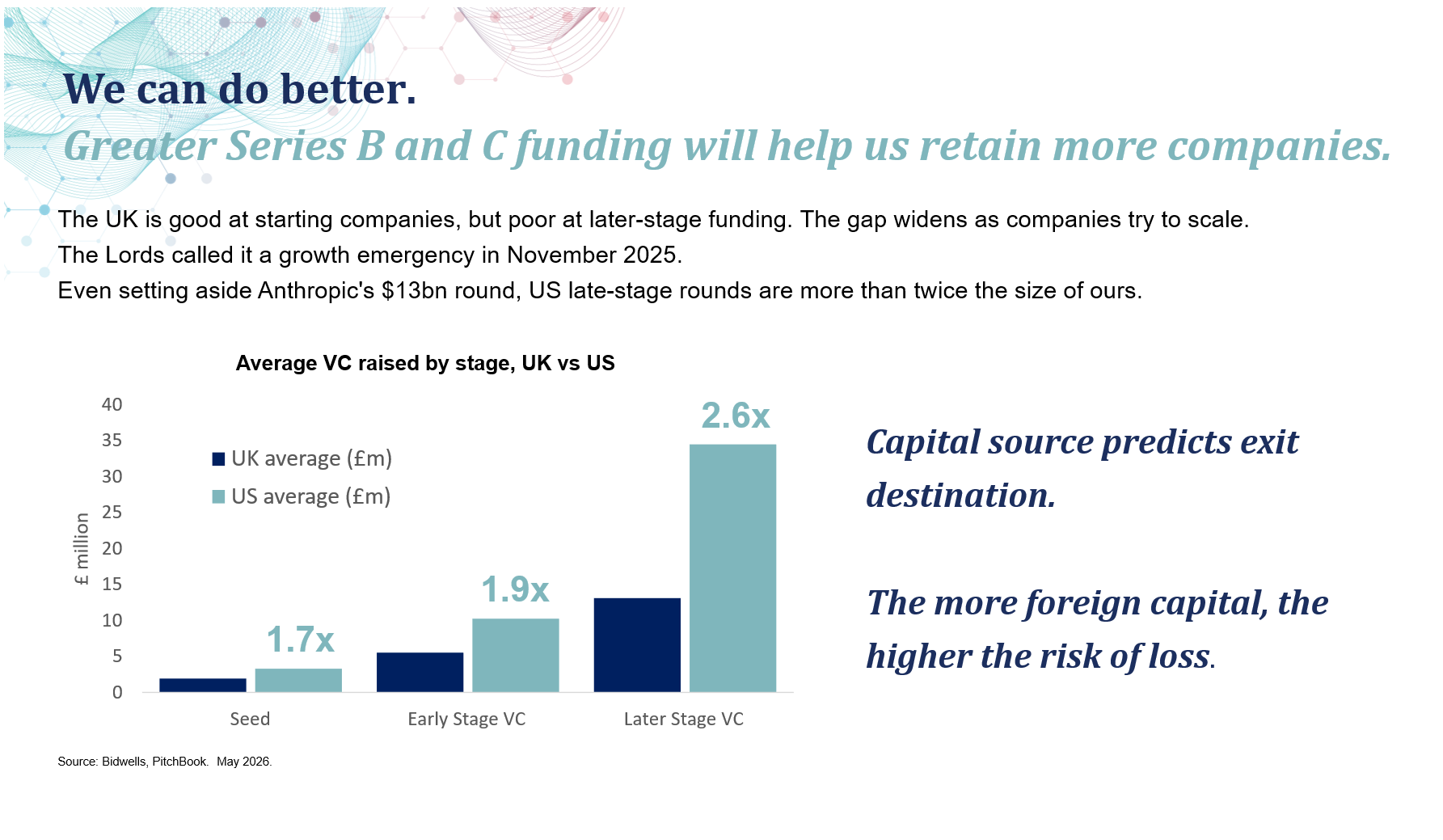

Adolescence is tricky

While the UK is good at incubating new businesses, a lack of finance at later stages when they are growing sales but are not yet profitable means that they often fail to develop into large domestic, or even global companies. Late stage scale-up businesses in the UK attract less than half the capital of their peers in the US.

Joint research by Bidwells and Beauhurst sharpens the picture. Of every £1 of growth-stage capital raised by UK university spin-outs since the start of 2022, just 8 pence came from rounds funded entirely by UK investors. Not a single growth-stage round above £75 million has been funded by UK capital alone. The dependence on foreign capital at growth stage is structural, not cyclical, and it is widening. We will publish the full analysis in a forthcoming paper.

The Lords' November 2025 report Bleeding to Death sets out four recommendations:

Pension reform. Enforce the Mansion House Accord through the Pension Schemes Act 2026, requiring DC pension funds to allocate a minimum share of assets to UK private capital, including venture.

Institutional consolidation. Bring Innovate UK, the British Business Bank and the National Wealth Fund into a single coherent investment architecture, rather than the fragmented current arrangement.

SME procurement targets. Mandatory percentages for government departments awarding contracts to UK SMEs — anchor demand that helps companies build to scale on home revenue.

London Stock Exchange (LSE) reform. Close the persistent valuation gap with the US which drives UK spin-outs to list in New York.

What runs through these is twofold: more UK capital and a UK listing venue that actually competes. Neither lever works alone. Even UK-funded companies will choose to list overseas while London trades at a 20% discount to New York. Listing reform alone delivers nothing if there is no domestic venture capital to fund the rounds beforehand.

The Government is responding

To be fair to government, the picture is more favourable than the Lords' diagnosis might suggest. Real money is being committed, regulations are being reformed and infrastructure is being built. Three lines of action stand out.

Public R&D anchors. LIBRTI at Culham, the Health Data Research Service at the Wellcome Genome Campus, a ten-year commitment to the National Quantum Computing Centre at Harwell, and the Swindon drone testing facility (525,000 sq ft, one of Europe's largest). These facilities will pull in private sector investment.

Business-friendly regulation. The government has simplified the rules for clinical trial and agreed that the NHS will pay higher prices for new drugs. It has also taken a principles-based approach to AI regulation which is more flexible than the EU's. The Automated Vehicles Act 2024 means the UK will be the first in Europe to allow driverless vehicles.

Infrastructure. The government is planning to restrict the use of judicial review to delay new infrastructure projects. It has also announced AI Growth Zones with fast-track planning and prioritised grid connections. Planning reform is now central to the innovation agenda, not adjacent to it.

We are not too small to be ambitious

We need to stop using size as an excuse to temper our ambition. Switzerland has nine million people, and produces Roche and Novartis. Denmark, six million, produces Novo Nordisk. Israel, ten million, has more than twice the unicorns of the UK. So what does implementation of today’s policy ambition actually produce?

Firstly, a top-tier, specialist economy. The UK is already there in life sciences, AI, fintech. The challenge is to hold on to these positions and add leading positions in other sectors. The scale-up gap could close substantially if the Mansion House reforms take effect, leading to a new cohort of UK companies with global scale. Existing innovation clusters in Cambridge, Oxford and London would continue to expand and emerging clusters around public R&D anchors would reach critical mass. None of this is wishful thinking. It is within our reach if the macro reforms on pensions, government procurement, planning, regulation, etc already announced are delivered.

However, a genuine global powerhouse requires more. It requires being more ambitious with domestic private capital and it requires sustained public investment in frontier R&D and public anchor research facilities. In addition, it requires an adequate supply of the specialist R&D space, housing, skills training and infrastructure which enable a cluster to prosper.

Ideally, these supporting elements should be built ahead of demand rather than in response to it. Without them the risk is that the cluster becomes increasingly expensive and uncompetitive and that growth stalls as new businesses and workers go elsewhere. The Ellison Institute of Technology's £890m commitment at The Oxford Science Park, and DeepMind's growth from 75 to over 1,000 people in London, illustrate what can be achieved if the right local conditions are in place.

The potential gains from commercialising and keeping control of research started in UK universities and research institutes are substantial. A new cohort of major UK companies in life science, tech and other knowledge intensive industries would increase employment and living standards, not only in those sectors, but also in the wider economy. It would also boost taxes and take some of the pressure of government finances.